{kind=link}

What Is a FICO Score?

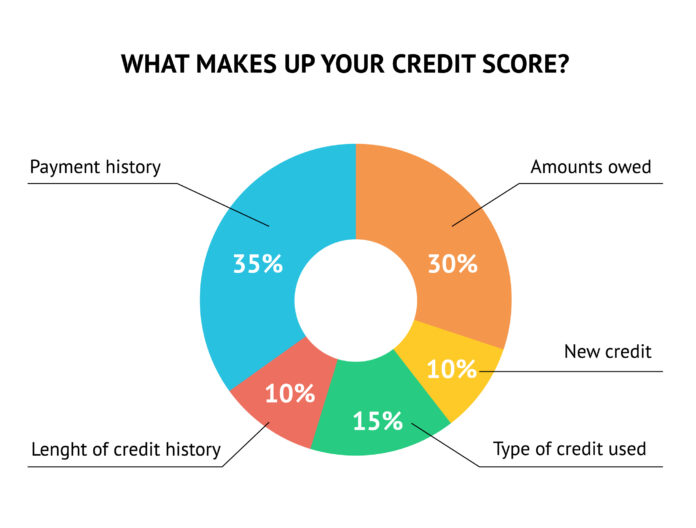

Most adults are familiar with FICO scoring, or have at least heard of the FICO Company. This is a type of scoring that utilizes a three-digit number to inform lenders how likely a consumer is to pay back the loan, or line, of credit they borrow. This number is based off of important information within the individuals personalized credit report. The three digit FICO scoring allows lenders the ability to know how likely the person is to repay the amount of money they are requesting to borrow. The scoring effects the amount being lent, the amount of time the customer will have to repay the line of credit, and the interest rate.

Who Is FICO

Founded in 1956, FICO, which stands for Fair Isaac Corporation, formed a company that focused on credit scoring services through the usage of data analysis. The company now assists businesses in over 90 countries to make appropriate lending decisions, reach higher growth levels, and make profits, all while maintaining customer satisfaction. Like all business models in order to stay current and relevant with the ever-changing world; FICO has also have to evolve over the years and update their FICO models. In 2020, the FICO Corporation launched a newest method for scoring individuals’ credit known as FICO Score 10. This is the latest version meaning there have been nine previous models prior to the FICO 10 release.

How Does the New FICO Model Work?

FICO is known to update their models for scoring around every five years. The algorithms must be analyzed and updated frequently in order to best predict risks. This new FICO 10 and 10T versions are the first time the company has offered two versions of the scoring model. Previous models would simply take a look at current account balances and generate a number. The updated version will actually review consumers overall account balances and any missed payments within the span of the last 24 months. However, consumers may begin to see a slight drop in their credit scores with the newest version. Experts estimate the drop should not be more than a 20-point decrease at maximum. This may be due to the fact that the new FICO version places more weight on delinquencies that have occurs in the past two years more than previous models. Additionally, FICO has announced that they also intend to flag consumers that have applied for personal loans due to the higher risk involved. Personal loans have been found to be the fasted growing debt type in the United States in a study completed in 2019. Overall, the new model is all encompassing because it takes into account the account balances for the previous 24-plus months and not simply looking at recent account balances. The FICO 10 and 10T do vary slightly as explained below.

FICO 10

This new model evaluates consumers credit card debt utilization ration more heavily than previous versions. With FICO 10, consumers are rewarded with little to no credit card balance but it does actually hinder borrowers with high relative balances. In addition, this new model places more weight on late payment history. Individuals that tend to make late payments each month should also expect to see a decrease in their scores, possibly more than predicted.

FICO 10T

The FICO 10T varies slightly because it includes “trended data” that occurred over the previous 24 months. Basically, it provides FICO with data to see if the consumer has been paying down debt or simply racking up new charges. The new model also focuses on keeping the debt down. Therefore, if consumers decide to consolidate credit card debt through a personal loan it would not be wise to charge the credit card up again because the new model will ultimately penalize the consumer.

What Does the New Model Mean for Consumers?

There is some hesitation to be expected when any new model is released to companies. However, this new version is much more accurate and is expected to provide consumers with good credit a boost in their score. The new model will be helping individuals that have good credit score by helping them achieve the score they deserve because of the accuracy. Even a slight increase in a credit score can help a borrower secure lower fees and interest rates. FICO is estimating that some credit card lenders could potentially reduce defaults by around 10% and auto lenders could reduce rates by around 9% when the new FICO model being utilized. For mortgage lender, borrowers could stand to see upwards of around 17% of a reduction. This new version will need to be reviewed by lenders and then the company will notify borrowers if they opt to implement the new model. However, along with the benefits, individuals will need to take extra precautions in order to avoid missing any payment as this will most likely result in a decrease for their credit score.

How To Get a Higher Score on the FICO 10 and 10T Model

Most importantly, consumers will need to keep a few key items in mind when trying to work toward a higher score on the FICO 10 and 10T model. First, consumers will want to pay down their credit card balances. If consumers are observed having consistently high balances and or raising balances this can signal financial difficulties to lenders. Borrowers are also advised to not miss a payment. Secondly, it is important that if a customer is consolidating their debt they need to be sure to avoid racking up the credit card balances in the future, as it will hurt their score. Again, with how the data is collected and analyzed; a missed payment will now lower scores. Lastly, it is recommended that individuals start an emergency fund. Ultimately, many people tend to turn towards credit cards during emergencies or difficult financial times. However, by utilizing credit cards to relive immediate financial burdens can end up decreasing a credit score.

Why Should Credit Scoring Be Important to You?

In general, an individual will need to apply for a line of credit at some point in their life. Whether the credit be required through financing a new car, applying for a credit car, or purchasing a home; a credit check will have to be ran prior to any loan being extended to an individual. Therefore, it is important for consumers to build their credit but to not place themselves in debt long-term. No matter what model the credit is being run through, consumers will need to have a decent history in order to continue to borrow.